M&A Deals

2015 Update

For the first two months of 2015, M&A deals have maintained similar volumes to the first two months of last year (2014).

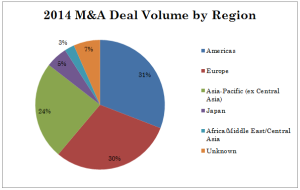

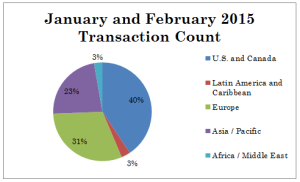

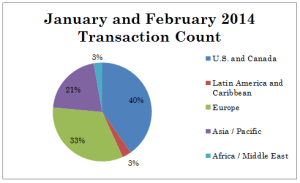

In terms of the number of transactions, 10,465 transactions were completed in the first two months of this year versus 10, 915 deals n the first two months of last year. The reduction is statistically insignificant. Interestingly, as you'll note in the charts below, the number of transactions by region was nearly identical between the two time periods. With transaction count, the number of transactions in Europe was two percent lower while the number of transactions in Asia was two percent higher.

M&A Deals - 2015

M&A Deals - 2014

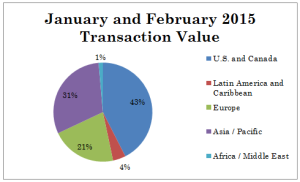

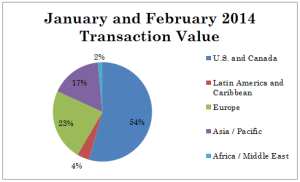

With regard to transaction values, approximately US$490.6 billion of transactions were completed in the first two months of 2015. In comparison, the transaction value for the first two months of 2014 was US$511.5 Billion. This was a slight decrease and because the number of transactions between the two relevant time periods actually decreased in the same period, it portrays a scenario where the average deal size increased from 2014 to 2015.

M&A Deals - 2015

M&A Deals - 2014

With regard to value in the first two months of 2015, M&A deals in Asia increased by approximately 82 percent compared to the first two months of 2014. This offsets a decrease in the value of transactions in the US, Europe, and Africa/Middle East. As you will note in the chart above, the percentage of US deals dropped from 54 percent in 2014 to 43 percent in 2015.

M&A Deals - Conclusion

Data is data and is always subject to revision, errors, and manipulation. That being said, M&A activity has been quite strong and is expected to stay that way for some time. There are always economic or political events that can have sudden impacts. No one knows exactly what will happen when the US Federal Reserve Bank starts to raise interest rates in the US. Buyers and sellers of companies both agree that they're hoping it won't have an impact.

Please click this button to view Versailles Group's Ebooks: