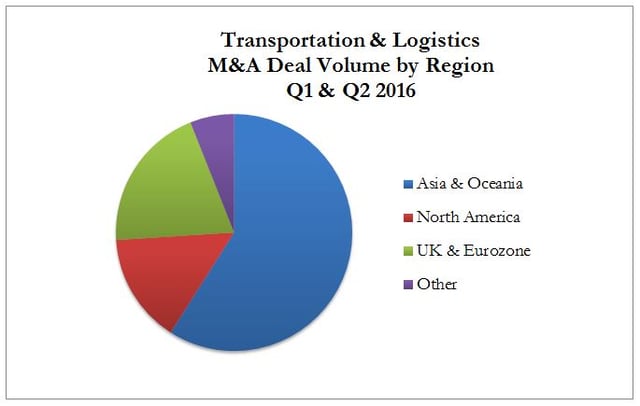

Mergers and acquisitions are an effective and efficient substitute for R&D for companies that need help combating shrinking market share or stagnant growth. In some cases, companies are confronted with fierce competition from startups and utilize M&A as a way to “outsource” R&D and leave the risk of innovation to startups that tend to excel at R&D. Many of these companies are skipping R&D almost entirely by acquiring other companies. This trend is true in almost all industries, and many of the transactions are cross-border.

The chart below depicts the top three sectors for cross-border M&A.

In recent months, Samsung has been actively involved in M&A deal making as a way to instantly build up its capabilities in emerging technologies such as mobile payments, cloud-based services, and artificial intelligence.

Samsung’s planned purchase of U.S. autoparts supplier Harman International Industries Inc. for US$8 billion in an all-cash deal instantly makes Samsung a major player in the world of automotive technology. It’s an excellent example of a company that is using M&A to expand. This deal will be the South Korean smartphone maker’s biggest acquisition in history.

M&A in general and cross-border M&A in particular is a well-proven way to enhance shareholder value, either by acquisitions or divestitures. While most of the press is focused on the large transactions, middle-market companies can also utilize this “tool” to make defensive or offensive acquisitions or divest businesses that no longer fit the company’s strategy.

The chart below demonstrates the growth of cross-border M&A deals from Q2 2016 to Q3 2016.

Versailles Group is a Boston-based investment bank that specializes in international mergers, acquisitions, and divestitures. Versailles Group’s skill, flexibility, and experience have enabled it to successfully close M&A transactions for companies with revenues greater than US$2 million. Versailles Group has closed transactions in all economic environments, literally around the world.

Versailles Group provides clients with both buy-side and sell-side M&A services and has been completing cross-border transactions since its founding in 1987.

More information on Versailles Group, Ltd. can be found at www.versaillesgroup.com.

For additional information, please contact

Founder and President

+1 617-449-3325

November 25, 2016