M&A Deals

Acquisitions

There are several reasons why companies make, or should consider making, acquisitions. Among the more important reasons are the following:

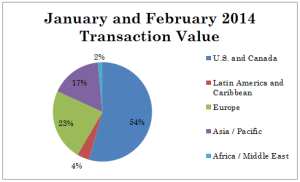

Accelerate market access for existing products. For example, for a non-US company, the US and Canada combined would provide exposure to one of the largest and most vibrant markets in the world.

Obtain skills or technology faster or at lower cost than they can be developed.

Acquire products in other geographies that can be manufactured and sold in the company's home territory.

Increase market share and/or reduce competition.

Diversify product portfolios or add entirely new products.

Achieve economies of scale for production, sales, etc.

Develop cross-selling opportunities.

Enable vertical integration.

M&A deals require focus and attention to detail. A well-experienced investment banker can help a company refine its objectives with regard to an acquisition and help them complete a successful transaction.

Over the years, many prospective clients have come to us with an idea that they'd like to acquire another company. In many cases, the idea hasn't been a bad one, but not worth pursuing. Some CEOs believe that an acquisition will fix an unprofitable or troubled business. Yes, that's possible, but not likely. In other words, one should consider acquisitions carefully, define the goals of acquiring a company, and then devise a strategy and tactics to achieve it. Buying something for the sake of it, will not increase shareholder value. And, certainly buying a company without carefully defined objectives will only exacerbate profitability or other problems at the acquiring company.